Blog

AWS-3 auction marks a U-turn in spectrum auction revenues

We put auction in context as prices pass an average of $1.82/MHz/POP

The FCC’s AWS-3 auction, once considered a sideshow before the repeatedly delayed 600 MHz incentive auction, has surprised the telecoms industry by attracting huge bids.

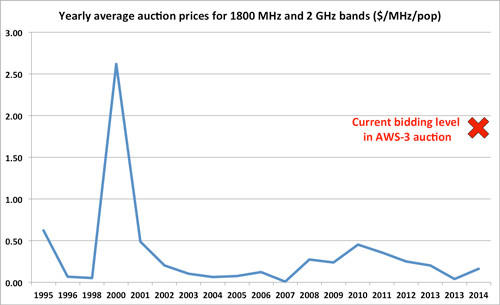

At the end of round 35 of bidding, a total of $37.5 billion had been offered for 65 MHz of spectrum in around 1.7 GHz and 2.1 GHz, which is equivalent to $1.82/MHz/POP. A glance at PolicyTracker’s Global Spectrum Database shows that the price marks a sharp rise from similar auctions in recent years.

The spectrum consists of four paired blocks encompassing 2 x 25 MHz (1755–1780 MHz and 2155–2180 MHz) and two unpaired blocks totalling 15 MHz (1695–1710 MHz). As is common in US auctions, bidders are buying individual licences for the country’s 880 Economic Areas (EAs) or 734 Cellular Market Areas (CMAs), depending on the particular block.

Our crude calculation belies significant variations between regions and bands. For example, a 2 x 10 MHz J Block licence for the “NYC–Long Island” EA now costs $2.4 billion, whereas a different 2 x 10 MHz G block licence in “Louisana 9” CMA will only set you back $1,300.

These high prices have been generated despite the fact that the successful bidders’ uplink operations will be restricted to low-power transmissions, and that operators will have to obey sharing arrangements with the band’s incumbents.

For perspective, in March this year, the FCC held an auction of 2 x 5 MHz in similar frequencies (1915–1920 MHz and 1995–2000 MHz) which cleared at the FCC’s reserve price, the equivalent of $0.55/MHz/POP. Data from the Global Spectrum Database shows that these results represent a significant spike when compared to average global auction revenues for spectrum in similar bands (1800 MHz and 2 GHz bands).

If these results were this year’s average revenue from the bands then it would not only represent a significant U-turn in the behaviour of mobile operators, but would also plot a U-shape on our diagram.

Toby Youell, PolicyTracker

27/11/2014

By |

PolicyTracker

Experts talk spectrum.

Listen Now

Spectrum Research Service

- Dossiers new

- Benchmarking new

- Spectrum database

-

Research notes