Blog

Weekly Wrap: European consolidation and its impact on spectrum holdings

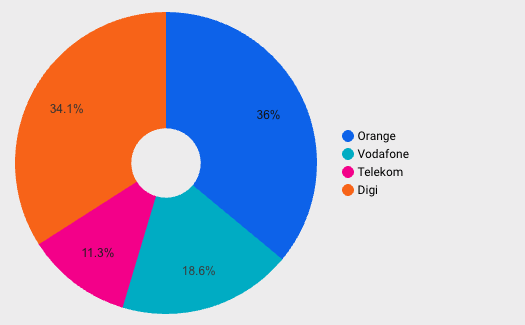

In-market consolidation in Europe is steadily continuing its course. This month, Telekom Romania's sale was approved by the Romanian Competition Council. The two biggest competitors will buy the operator's assets.

Vodafone Romania will acquire the core assets of Telekom Romania Mobile, including its employees, postpaid and business customers, retail stores, and technical infrastructure, which will strengthen Vodafone’s position in the country’s telecom market.

Digi Romania will buy the rights to certain radio frequencies, a selection of towers and equipment, as well as the entire prepaid mobile telephony business.

The deal remains subject to the final agreement of terms and approval from the National Authority for Management and Regulation in Communications (ANCOM), the Romanian telecom regulator.

To address regulatory concerns, Vodafone and Digi have committed to developing local networks, improving mobile coverage, and enhancing data quality. Both companies will continue providing access to their networks for mobile virtual network operators at competitive rates and will ensure Orange Romania’s continued access to co-location services on mobile sites. Digi will also maintain Telekom Romania’s prepaid contracts under existing terms and continue offering these services to all consumers.

The commitments made as part of this transaction will be monitored for up to four years by an appointed trustee who will report to the Competition Council and coordinate with ANCOM. Any failure to respect the conditions could result in fines of up to ten per cent of the company’s previous-year turnover.

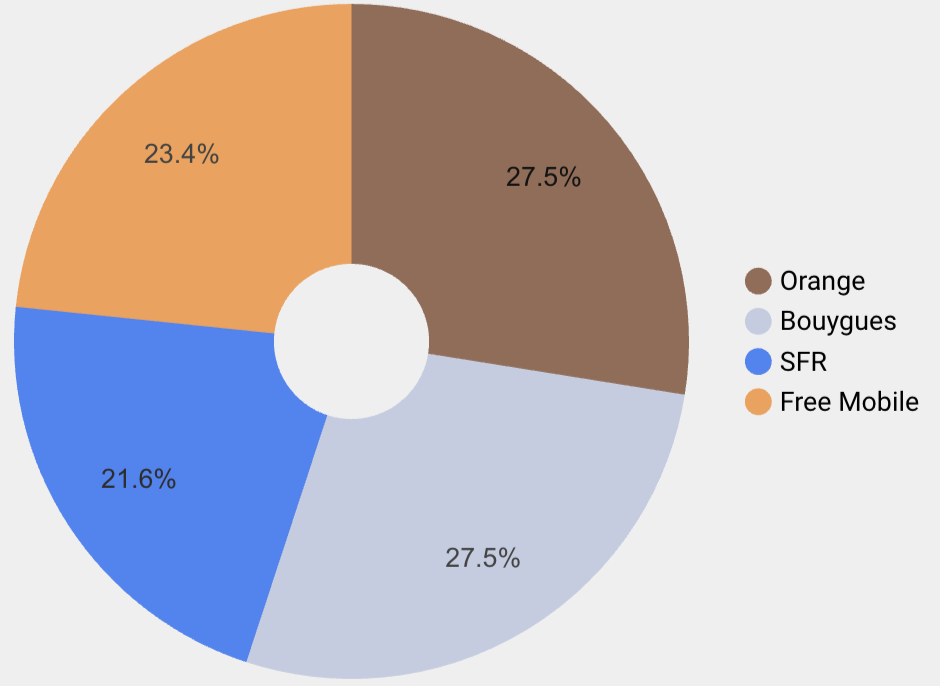

Elsewhere in Europe, in France, speculation about the sale of SFR has intensified in the course of this year amid parent company Altice’s efforts to reduce its debt. According to reports from the Financial Times, Altice is considering breaking up SFR and selling it in parts. Valuations for SFR are estimated at EUR 21 – 30 billion.

France’s three main telecom rivals, Orange, Bouygues Telecom, and Iliad-owned Free, are reportedly in talks to divide SFR’s assets among themselves, potentially with support from private equity firms looking to finance the deal. The rationale is that dividing SFR could maximise overall value while addressing regulatory concerns around reducing competition in France’s four-operator market.

It’s noteworthy in these two cases that operators are choosing to divest their assets among themselves, instead of transferring them to a new entrant. The recent VodafoneThree merger in the UK is another example of this, as Vodafone voluntarily sold spectrum to VM/O2 to avoid becoming an overly dominant spectrum holder.

Historically, we’ve seen competition authorities mitigating mergers by introducing new players through spectrum divestments. Last year, for example, as a condition for the MasOrange merger, the regulator asked the companies to divest spectrum assets to a new market entrant (Digi, in this case). In 2014, 1&1 entered the German mobile market through a spectrum divestment following the merger of Telefonica and e-plus.

So far, this change in competition policy is largely being driven by national member states. As we approach the publication of the Digital Network Act, the European Commission may also change its tune.

Here’s what PolicyTracker covered this week:

- AST SpaceMobile, which is planning a low Earth orbit satellite network using licensed mobile spectrum for direct-to-device connectivity, is facing strong blowback from ham radio operators

- US satellite and mobile provider EchoStar has agreed to sell some of its most valuable spectrum assets to AT&T in what appears to be the largest private spectrum transfer in history

- In our latest podcast episode, Wi-Fi Alliance CEO Kevin Robinson explains the Big Beautiful Bill and the latest 6 GHz developments around the world

- Mobile network operators say that the Australian regulator’s proposed renewal fees have overvalued spectrum licences by billions of dollars

By |

Laura Sear

Laura is the News Editor at PolicyTracker. Her work is focused on spectrum policies in Europe. She has previously written for The Guardian, Deutsche Welle and several Belgian publications such as the VRT and Knack. Laura is fluent in English, Dutch and French and has a master's degree in International Journalism from City University of London.

Experts talk spectrum.

Listen Now

Spectrum Research Service

- Dossiers new

- Benchmarking new

- Spectrum database

-

Research notes